Joe Zidle: Duration Will Be Central to This Historic Recovery

The year is 1984. President Reagan intensifies the Cold War with comments about “outlawing Russia,” the first Mac goes on sale, and The Karate Kid sweeps the leg. In 2021, the U.S. again faces increased tensions with a rising power, the iPhone has more processing power than Apollo-era spacecraft, and Daniel LaRusso and Johnny Lawrence continue their rivalry, this time in Cobra Kai.

1984 was also a big year because that was the last time the U.S. economy’s growth rate exceeded 7%. And as the pace of vaccinations increases this year, so does my conviction that the U.S. has its strongest economic growth since at least 1984. Fiscal spending and monetary policy are creating a uniquely synchronized start to an expansion. Normally, a recovery begins on more tenuous footing. Households require time to rebuild income and savings before they can spend. Corporations need demand to increase before they can repair balance sheets and rebuild profits. And state and local governments struggle to recoup lost tax revenue. But in this front-loaded recovery, households, corporations, and state and local governments are flush with record cash and poised to simultaneously contribute to growth.

An historic recovery like this at such an expedited pace comes with unique investment considerations that require careful positioning. Current market leadership and portfolio allocation assumptions will be challenged as surging growth results in tightening labor markets, inflationary conditions, and a steepening yield curve. The coming quarters may prove to be an inflection point for assets that can hedge against or benefit from these conditions.

Labor, Inflation, and the Yield Curve

Tight labor markets The number of people out of work today remains nearly double that of pre-COVID levels, and weekly jobless claims continue to hover above one million. It’s perhaps counterintuitive, then, that companies are reporting serious challenges in finding qualified workers. The Federal Reserve’s most recent Beige Book described labor shortages across most regions, with the most acute shortages in low-skill jobs. An unemployment rate of 6.2% would seem to imply slack in the labor markets, but a structurally smaller labor force tells a different story.

Higher demand, fewer workers I have highlighted several issues causing people to exit the workforce. Some issues are shorter-term, like childcare, which the resumption of in-person schooling should mitigate. Others are longer-term, such as generous government transfers that could make certain lower-paying, low-skill jobs less appealing. As the economy reopens and this recovery unfolds, we could see a record increase in demand for services at the same time that companies can’t hire enough people to scale up capacity. In a record-setting year with many inflationary pressures, wage gains are something to watch.

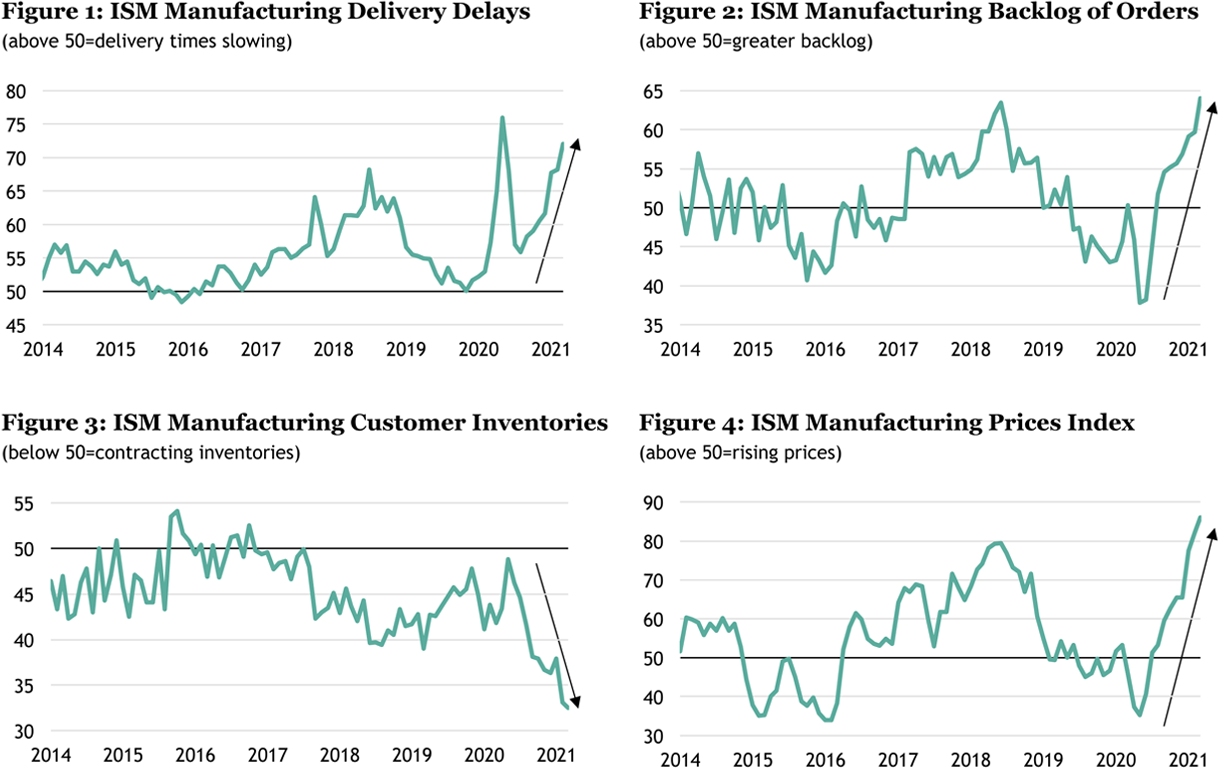

All types of inflation are emerging Wage inflation is generally considered “sticky”: Once gains are made, they tend to be long-lasting. But that’s not the only kind of inflation emerging. Renewed demand for goods and the logistical challenges of resuming global trade continue to wreak havoc on supply chains. This has led to delivery delays, depleted inventories, and increased prices, as highlighted in Figures 1 through 4.

Source: Institute for Supply Management (ISM) and Bloomberg, as of 2/28/21.

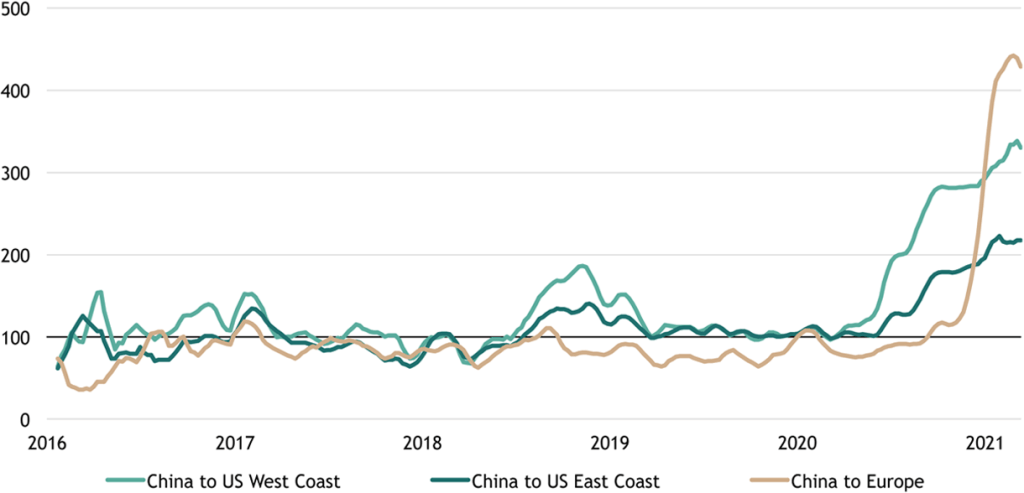

The ports of Los Angeles and Long Beach provide an example. Together, these ports handle more containers per ship call than any other port complex in the world and account for 31% of the U.S.’ market share of waterborne import cargo, making their activity a bellwether for trade.1 Since Q3 2020, global manufacturing and trade have ramped back up as economic recovery began. Increased shipping volumes have squeezed ocean capacity and significantly increased ocean freight costs, with many trade lanes’ prices spiking to their highest levels since 2016, as shown in Figure 5. Logistics networks have been challenged to accommodate this significant surge in supply-side activity. Each link of the supply chain is interdependent on other links working optimally, and if one link becomes dysfunctional, the compounding effect slows the full logistics chain. The consequences of a stretched supply chain have been particularly visible in the record-high ship gridlock situation in U.S. and global ports during the past few months.2

Supply chain imbalances, combined with tight labor markets, are expected to push CPI and PCE readings to their highest levels since summer 2018.3 These dynamics are likely to continue to drive up long-term interest rates, with implications for a steepening yield curve.

Figure 5: China Ocean Freight Value

(indexed to 100 as of 12/31/19)

Source: Freightos and Bloomberg, as of 2/28/21. The Freightos Baltic Index is the leading international Freight Rate Index, in cooperation with the Baltic Exchange, providing market rates for 40′ containers (FEUs). https://fbx.freightos.com/

Steeper yield curve is normal In the last three recoveries, the curve steepened by an average of 180 basis points (bps) from the recession’s start to 24 months into the subsequent recovery.4 But this time, the steepening will likely play out much more quickly, given the powerful, coordinated forces driving the recovery. The Fed may eventually intervene to prevent 10-year Treasury yields from rising unchecked and weighing on growth. Even so, I’m of the view that, while the 10-year yield’s floor is in place, we’ve yet to find its ceiling, a point Fed Chair Powell echoed repeatedly in recent weeks. With the short end of the yield curve anchored to zero by Fed policy and cost and wage pressures pushing up the long end, look for further steepening.

Interest Rate-Proofing a Portfolio

If inflationary pressures continue to push long-term interest rates higher, the traditional playbook says that investors should shorten the duration of their fixed income holdings to reduce duration risk. This strategy remains true in the current environment. However, investors should also be aware of the potential for a change in leadership in other asset classes, including equities and real estate.

Equities Years of secularly low and falling inflation and bond yields created winners out of some of the longest-duration assets, including the most speculative stocks in equity markets, which we can consider “long duration.” Investors in the stocks of these pre-revenue companies and unicorn start-ups expect to be compensated by cash flows that materialize far in the future. When rates rise, it’s more expensive to discount far-distant cash flows back to the present because investors sit out other opportunities while they wait for their unicorn to turn a profit. As yields steepen, investors should carefully reexamine their thesis for non-earners, especially among those who benefit the most from cheap capital. Assets with high current cash flow and growth have the potential to outperform.

Real estate Cash flow flexibility, comfortable cap rate spreads, and constrained supply can make private real estate an attractive asset class in today’s higher interest rate environment. To discuss these points and more in a special contribution this month, let’s turn to one of our experts.

Real Estate in an Inflationary Environment

by Nadeem Meghji, Senior Managing Director, and Head of Real Estate Americas, Blackstone

One of the most frequent questions we receive is how to think about real estate in the context of a growing economy accompanied by higher inflation and rising interest rates. The good news is that real estate can be an excellent hedge against inflation. For the right assets, in the right markets, real estate has performed well in rising-rate environments, particularly when economic growth is strong. However, sector and geographic selection are important.

Real estate can offer dynamic cash flows Unlike traditional bonds that generate fixed cash flows, the income streams from real estate can rise over time. In an inflationary environment, market rent growth for most real estate assets will accelerate. In this context, prioritizing assets with shorter lease durations in sectors with strong underlying growth fundamentals can result in faster translation of higher market rents into underlying operating cash flows. Hotels represent the most extreme example of this because they effectively have one-night leases and rate increases can be quickly implemented. Other sectors, including apartments and warehouses, often have shorter-duration leases as well, allowing for greater near-term cash flow growth in an inflationary environment. All of this can help offset the potential valuation impact of higher borrowing costs and rising cap rates.

Not all properties will perform similarly Bond-like assets that have long-term leases with limited rent resets are more susceptible as rates rise. Also, sectors suffering from weaker tenant demand, like certain U.S. regional malls and urban office buildings, may not be able to command near-term rent increases that can keep up with inflation. As I survey our own portfolio for reference, we have largely avoided these more vulnerable assets while concentrating in fast-growing sectors. For example, the industrial sector is benefiting from explosive growth in e-commerce demand. Lab offices are poised for growth due to a revolution in biotechnology. Hollywood studios and creative offices are buoyed by the growth in global content creation. And suburban apartments in the Sunbelt are capitalizing on strong demographic tailwinds and a housing supply shortage.

Cap rates have room for rates to rise The relationship between cap rates and a risk-free rate of return is important. Today, real estate cap rates and valuations appear quite reasonable when compared to 10-year Treasury yields. The major real estate sectors currently trade at an average cap rate of about 5.4%5, which represents a spread of about 370-bps to the 10-year.6 This spread is significantly wider than the historical spread, which has averaged about 270-bps over the last 35 years. Given this starting point, rising interest rates may not necessarily result in a commensurate rise in cap rates. Most recently, we saw this phenomenon in 2012–2013 and 2016–2018, two periods when interest rates rose but cap rates remained relatively flat or even declined. In fact, in each of the four cases of rising interest rates over the last 25 years, commercial real estate values rose in the aggregate.

Limited supply will support valuations Another factor impacting real estate appreciation is new supply, which historically has been an important risk factor in cycles. The encouraging news is that supply is generally in check. For example, even in the industrial sector, which is benefiting from tremendous demand from tenants and investors, annual new supply equates to approximately 2% of inventory in the U.S., in line with the 30-year average.7 To the extent that we enter an inflationary environment this year, increases in the cost of land, construction, and labor are likely. These increases will make new supply more costly and, in some cases, less financially feasible. In fact, over the past six months, replacement cost increased by 7%–10% for apartments, office buildings, and warehouses in many major markets.8 Less supply will enable existing assets to maintain higher occupancies and stronger pricing power, which will help support values.

Labor costs require close attention A key aspect of inflation is rising labor costs, which can put pressure on operating margins. While most real estate sectors have high margins and modest exposure to labor costs, certain operationally intensive sectors like hotels and senior housing assets are more vulnerable. This does not mean that these sectors should be avoided, but rather that any underwriting needs to recognize a more significant labor component and reflect realistic expense growth assumptions. For example, a strong cyclical recovery in leisure-oriented hotels over the next several quarters would lead to strengthening demand, which in turn should result in improving pricing power for hotel owners, potentially offsetting the impact of rising labor costs.

In an investment environment where rates and inflation could rise, real estate can represent a potential place to produce outsized returns. The key is selecting the right assets with the right business plan while avoiding sectors experiencing secular headwinds and assets with bond-like cash flows. Also, investors can take advantage of the current rate environment by borrowing on a long-term basis and fixing interest rates, much as we have done in our long-term, core-plus vehicles. This can help mitigate the impact of rising rates and provide for more predictable cash flows over time. Within the right sectors, real estate can provide cash flow yield and growth, with the potential downside protection that hard assets afford.

With data and analysis by Taylor Becker.

- Port of Los Angeles, as of 2020. https://www.portoflosangeles.org/business/statistics/facts-and-figures

- Freight Waves, as of 2/11/21. https://www.freightwaves.com/news/new-video-shows-massive-scope-of-california-box-ship-traffic-jam

- Bloomberg consensus forecasts, as of 3/22/21. “CPI” is the year-over-year percent change in U.S. CPI for urban consumers, not seasonally adjusted. “PCE” is the year-over-year percent change in the U.S. GDP personal consumption price index, seasonally adjusted.

- Federal Reserve Board of Governors. Based on the spread between constant maturity 10-year and 2-year nominal Treasury yields. Recession periods are defined by the National Bureau of Economic Research.

- Green State Advisors, as of 3/1/21. Major sectors include multifamily, logistics, mall, office, and strip centers.

- Based on daily 10-year UST rate, as of 3/22/21.

- CBRE-EA, as of 3/31/21.

- Blackstone proprietary data, as of 3/31/21.

The views expressed in this commentary are the personal views of Joe Zidle and Nadeem Meghji and do not necessarily reflect the views of The Blackstone Group Inc. (together with its affiliates, “Blackstone”). The views expressed reflect the current views of Joe Zidle and Nadeem Meghji as of the date hereof, and none of Joe Zidle, Nadeem Meghji nor Blackstone undertake any responsibility to advise you of any changes in the views expressed herein.

Blackstone and others associated with it may have positions in and effect transactions in securities of companies mentioned or indirectly referenced in this commentary and may also perform or seek to perform services for those companies. Blackstone and others associated with it may also offer strategies to third parties for compensation within those asset classes mentioned or described in this commentary. Investment concepts mentioned in this commentary may be unsuitable for investors depending on their specific investment objectives and financial position.

Tax considerations, margin requirements, commissions and other transaction costs may significantly affect the economic consequences of any transaction concepts referenced in this commentary and should be reviewed carefully with one’s investment and tax advisors. All information in this commentary is believed to be reliable as of the date on which this commentary was issued, and has been obtained from public sources believed to be reliable. No representation or warranty, either express or implied, is provided in relation to the accuracy or completeness of the information contained herein.

This commentary does not constitute an offer to sell any securities or the solicitation of an offer to purchase any securities. This commentary discusses broad market, industry or sector trends, or other general economic, market or political conditions and has not been provided in a fiduciary capacity under ERISA and should not be construed as research, investment advice, or any investment recommendation. Past performance is not necessarily indicative of future performance.

For more information about how Blackstone collects, uses, stores and processes your personal information, please see our Privacy Policy here: www.blackstone.com/privacy.