Joe Zidle: Fading Tailwinds, New Opportunities

I got a kick out of the recent announcement that California’s Disneyland is selling a $100 sandwich at the theme park’s new Avengers Campus. It sounds good, with rosemary ham and sun-dried tomatoes layered on toasted focaccia. We’ll see what the market is for this massive sandwich, which allegedly feeds 6 to 8 people. But when people have more money, they’re generally willing to pay more for things. We call that demand-pull inflation. Expect to see more of it.

Inflation is just one of many macro variables that will behave differently during this cycle compared to the last one. From March 2009 to February 2020, interest rates, corporate taxes, and company costs all fell, driving historic earnings and profit margin gains. Such benign macro conditions were the bread and butter (or sun-dried tomato) of the “everything” rally, in which beta drove up asset returns across the board. This time, all three variables are poised to rise.

Because the new bull market will feature fundamentally different macro drivers compared to the last cycle, investors need a fresh perspective to achieve a successful portfolio strategy. In particular, traditional fixed income is currently priced for perfection and vulnerable to the coming macro environment, which I expect to feature higher inflation, rising rates, and more difficult operating conditions. Against this backdrop, I brought in Dwight Scott, global head of Blackstone Credit, to give his unique insights into the risks and opportunities in today’s credit markets.

This Time is Different — No, Really

“The four most dangerous words” This is famously how the late Sir John Templeton referred to the phrase “this time is different.” Even so, I expect the real economy to achieve escape velocity during this recovery in a way that it didn’t after the Global Financial Crisis (GFC). Thanks to the outsized policy response, corporate and consumer balance sheets have plenty of cash on hand to spend at the start of this cycle. That spending will likely beget strong labor demand and higher wages, fueling further consumption—the so-called “virtuous cycle.” As a result, the Fed will achieve its dual mandate of moderately higher inflation and a strong labor market, enabling it to take its foot off the money pedal in a way that it couldn’t over the last decade.

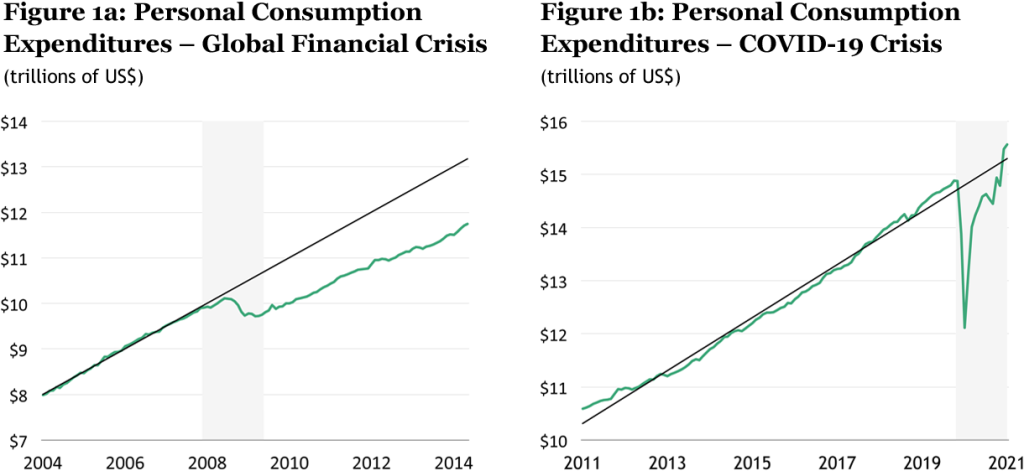

Figures 1a and 1b highlight the extent to which consumer spending was impaired following the GFC. In fact, over the decade-long recovery, spending never returned to its pre-crisis trend. As a result, the real economy was left with slack. Compare that to the post-COVID period: We’ve already exceeded the pre-pandemic consumption growth trend—and that’s with $2 trillion in excess savings still on the sidelines. This spending not only argues for a self-sustaining expansion, but it also supports the idea that the economy will soon bump up against production capacity. The slack in the U.S. economy is quickly being eliminated.

Source: Bureau of Labor Statistics and Blackstone Investment Strategy, as of 4/30/21. Shading represents recessions. Solid black line represents the trend from the beginning of the time period shown until the beginning of the recession in question.

Inflation for longer Given the amount of cash in the economy, investors must prepare for the possibility that the inflation we’re currently seeing is not transitory, sandwiches included. Treasury breakevens, which measure the difference between nominal yields and TIP yields, are an indication of market inflation expectations. Breakevens are signaling that investors expect high price growth for the next 3 to 5 years before returning to about 2% over the long run. Also, long duration, low coupons and massive inflows into fixed income markets and investment in speculative stocks tell me that investors haven’t prepared their portfolios for the possibility that inflation will run hotter this cycle than it did over the past decade. If persistent components of inflation like wages and rents continue to rise, then price growth could be with us for a while.

Interest rate risk real In my view, the 10-year Treasury yield has already found its floor, being unlikely to fall below 1%. We don’t yet know where the ceiling is, but it is certainly above the 10-year’s current level around 1.5%. In the short term, yield movements might be volatile, but the moves are less useful as a signal today than they were in the past. Bond prices are being inflated by the Fed’s quantitative easing program, and as such, serve to distort the signal of what bond markets are pricing in for growth and inflation. That’s why we would fade the 10-year’s recent leg downward and continue to think the secular move is higher. As a result, investors should reconsider their investment positions to protect against the disproportionate risk of higher rates, especially in the face of rising inflation.

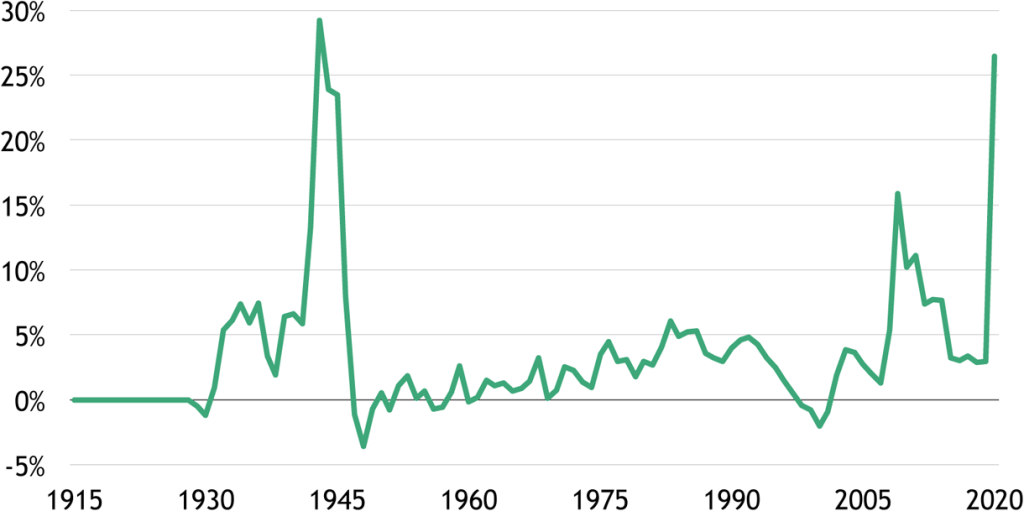

Policy response shrinks In the next few quarters we will pass peak liquidity as the strongest coordinated fiscal and monetary policy since World War II begins to wind down (see Figure 2). As much as markets wish it weren’t so, eventually the Fed will taper its purchases, reduce the size of its balance sheet, and raise interest rates. Also, no fiscal policy during the new cycle will rival the immediate government transfers distributed during COVID. Congress is likely to pass President Biden’s proposed infrastructure bills, but with a much lower price tag than what the administration pitched initially. And even then, that spending will likely take about a decade to be disbursed.

Figure 2: U.S. Federal Deficit Plus Federal Reserve Balance Sheet Expansion

(percentage of nominal GDP)

Source: Office of Management and Budget, Federal Reserve Bank of St. Louis, Center for Financial Stability, Federal Reserve Board, Bureau of Economic Analysis, and Blackstone Investment Strategy, as of 12/31/20.

Portfolio Preparation for the Brave New World

In light of these dynamics of strong inflation, higher rates, and tighter liquidity, investors must look for innovative ways to earn returns in this new cycle.

Lower valuations in equity markets The threat of higher interest rates, taxes, and costs will crimp valuations. I expect a secular earnings growth rate for public companies that’s half the pace of the last bull market. That means investors should look to invest in differentiated companies as Darwinian market forces reassert themselves.

In an inflationary environment, I expect outperformance from companies with pricing power that can pass on higher costs to customers. Also, companies that grow free cash flow should benefit as investors look for inflation hedges. A “K”-shaped recovery is possible across every sector in this scenario as discerning investors boost companies with strong fundamentals, while weaker companies struggle to attract capital. The future for pre-revenue companies and chronic non-earners will likely be more challenging. Weaker companies won’t be able to simply refinance their obligations at lower rates.

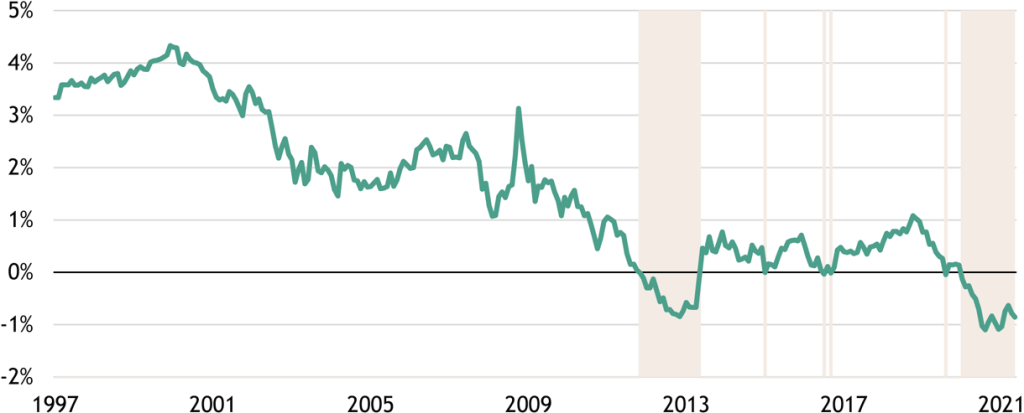

Outsized duration risk in fixed income markets The new cycle will require investors to identify corners of the market in which high returns are available without outsized risk. Since the pandemic began, real rates in the U.S. and around the world have been deeply negative, making the cost of capital historically low (see Figure 3). This anomaly should change course as the economy grows and interest rates grind higher. But higher rates mean lower prices and returns for traditional fixed income assets.

Figure 3: 10-Year U.S. TIPS Yields

Source: Bloomberg, as of 5/31/21. TIPS are Treasury Inflation-Protected Securities. Shading represents periods when 10-year U.S. TIPS yields were negative.

Given these challenges to portfolios, I tapped one of our experts to discuss private credit strategies and alternative investment solutions.

Private Credit in an Inflationary Environment

By Dwight Scott, Senior Managing Director and Global Head of Blackstone Credit

As the U.S. economy rushes headlong into the next phase of its recovery, credit investors are focused on a few particularly salient trends. First, return-to-work and the release of pent-up leisure spending provide an exceptionally strong economic background for borrowers across all risk classes, broadly reducing default risk. Second, today’s historically low rates reflect the end of a 40-year bull market in interest rates and create the risk of a reversal of those low rates in upcoming years. Third, rapid innovation in technology and business practices creates an investment environment in which identifying the best sectors, or “good neighborhoods”, is paramount in equity and credit strategies.

These trends highlight why I believe Blackstone Credit’s focus on private credit positions our investors particularly well in today’s market.

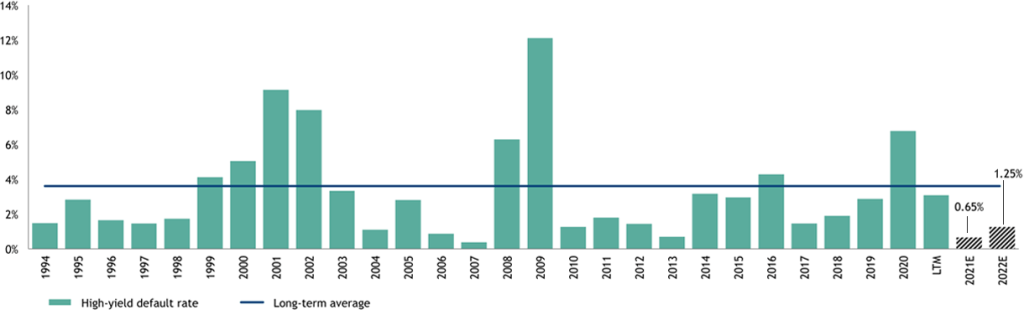

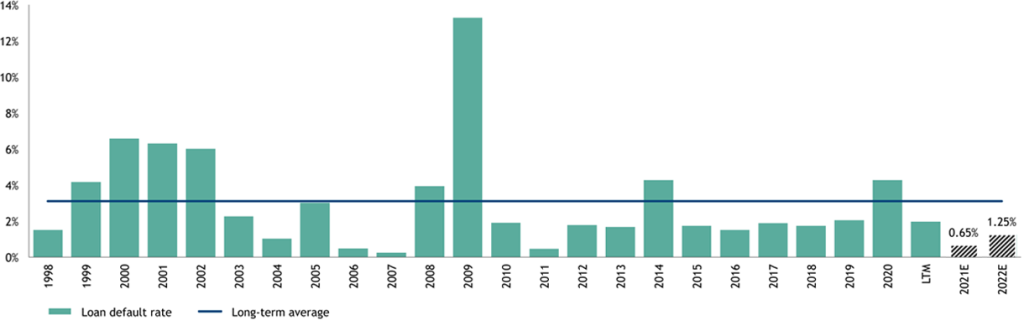

Strong conditions for borrowers As the recovery unfolds, the resultant increase in activity directly impacts borrowers by potentially increasing earnings, cash flow, and capital spending. These conditions create a benign default environment for credit investors. Rating agencies have upgraded more loan issuers than they downgraded in seven of the last eight months, with the upgrade-to-downgrade ratio running at 1.89 to 1.00 year-to-date. J.P. Morgan recently lowered its forecast for defaults in 2021 by U.S. high yield and loan issues to just 0.65% each, the lowest levels since 2011 (see Figures 4a and 4b).

Figure 4a: U.S. High-Yield Bond Default Rates

Figure 4b: U.S. Leveraged Loan Default Rates

Source: J.P. Morgan, as of 6/17/21. Default rates are par-weighted. 2014 default rates are ex-TXU Energy.

Expected continued earnings strength in the borrower universe over the next several quarters, lower leverage levels as cash flow forecasts improve, and excellent capital market access make this a credit-friendly environment. I expect private equity sponsors and other issuers to take advantage of this benign environment and come to market at record levels to finance their activities. Blackstone’s experienced origination team and low-cost fund structures allow us to see a high volume of deals and assist issuers in many different strategies.

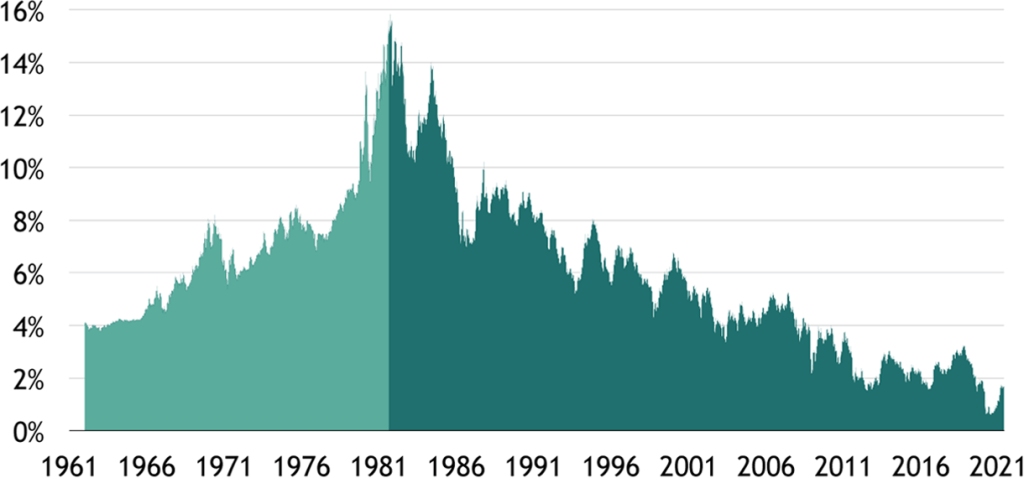

The end of an interest rate era The 40-year trend of falling interest rates in the U.S. provided many benefits to market participants, including lower interest costs to borrowers, higher valuation multiples for equity investors, and rising security prices for fixed income investors. As Joe discussed, there is significant risk that this tailwind reverses over the course of this business cycle. I believe the U.S. real economy will boom, inflation is poised to run higher, and the Fed will taper its asset purchases over the next few years and eventually unwind the size of its balance sheet.

For credit investors, this rates reversal means potentially higher interest costs to borrowers, lower valuation multiples for equities, and falling security prices for fixed income investors. Today, I think the rate risk inherent in longer duration securities may actually be larger than the credit risk in the underlying issuer.

Figure 5: 10-Year Nominal U.S. Treasury Yields

Source: Federal Reserve, as of 6/7/21.

One way to hedge duration risk is to invest in senior secured floating rate debt, which positions portfolios to benefit from the improving economic environment without taking longer-term rate risk. In fact, floating rate loans have the potential to benefit from rising rates as the underlying reference rate, like LIBOR, increases. Blackstone Credit has prioritized floating rate investments and private loans that are senior secured and protected by the core assets of the borrower. This means that we’re often protected well in case of an unexpected market disruption.

Sector selection is critical Credit investing can be both strategic and tactical in its approach to an investment opportunity. Strategic considerations include broad portfolio decisions such as sector choice, ratings allocation, and duration exposure. Tactical considerations include specific credit decisions like capital structure seniority, covenant structure, and call protection. While all these factors are critical when making credit investment decisions, strategic decisions about sector allocation are especially important in this era of rapid technological and business innovation.

Those who follow Blackstone have heard Jon Gray speak of the firm’s focus on investing in fast-growing sectors and high-conviction investment themes with strong secular tailwinds. This focus is no less important in credit, where companies in life sciences, last-mile logistics, renewables, digitization, and online content can potentially provide attractive risk-adjusted opportunities for lenders.

When it comes to credit selection, private strategies provide important benefits. Traditional liquid fixed income, which is a funds flow-oriented strategy, may struggle to deploy capital in a judicious way when funds are coming into the system. I think of it as a “buy and justify” strategy: If $100 million comes into your fund, you still have to deploy the money, even if you think that rates are likely to back up or you can’t find sufficient exposure to high quality sectors.

In contrast, in private credit, we can decide when to deploy capital, and how much to deploy. We don’t have to swing at every pitch; we can afford to wait for a strike right down the middle of the plate. This optionality afforded to illiquid credit strategies is one reason why private credit is attracting significant interest in the current environment.

A unique solution Private credit is well-suited to hedge investors against credit and rate risk, which will be an important consideration throughout this recovery. Portfolios can be structured with floating interest rate exposure, allowing investors to hedge duration risk and participate in any upside from higher interest rates because investments are pegged to a benchmark. Additionally, debt issued in private markets is often senior secured and sits higher within a company’s capital structure, which can provide downside protection in case the company struggles to fully repay investors. Finally, private credit investors can be selective, pursuing only those issuers in “good neighborhoods” where strong secular tailwinds may drive outperformance.

With data and analysis by Taylor Becker.

The views expressed in this commentary are the personal views of Joe Zidle and Dwight Scott and do not necessarily reflect the views of The Blackstone Group Inc. (together with its affiliates, “Blackstone”). The views expressed reflect the current views of Joe Zidle and Dwight Scott as of the date hereof, and neither Joe Zidle, Dwight Scott, nor Blackstone undertake any responsibility to advise you of any changes in the views expressed herein.

Blackstone and others associated with it may have positions in and effect transactions in securities of companies mentioned or indirectly referenced in this commentary and may also perform or seek to perform services for those companies. Blackstone and others associated with it may also offer strategies to third parties for compensation within those asset classes mentioned or described in this commentary. Investment concepts mentioned in this commentary may be unsuitable for investors depending on their specific investment objectives and financial position.

Tax considerations, margin requirements, commissions and other transaction costs may significantly affect the economic consequences of any transaction concepts referenced in this commentary and should be reviewed carefully with one’s investment and tax advisors. All information in this commentary is believed to be reliable as of the date on which this commentary was issued, and has been obtained from public sources believed to be reliable. No representation or warranty, either express or implied, is provided in relation to the accuracy or completeness of the information contained herein.

This commentary does not constitute an offer to sell any securities or the solicitation of an offer to purchase any securities. This commentary discusses broad market, industry or sector trends, or other general economic, market or political conditions and has not been provided in a fiduciary capacity under ERISA and should not be construed as research, investment advice, or any investment recommendation. Past performance is not necessarily indicative of future performance.

For more information about how Blackstone collects, uses, stores and processes your personal information, please see our Privacy Policy here: www.blackstone.com/privacy.