Joe Zidle: The Economic Growth Story Told Through Housing

Every summer around this time, my partner Byron Wien kicks off his series of Benchmark Lunches in eastern Long Island. I always find the dialogue to be engaging, thought-provoking, and packed with unconventional ideas. Like always, Byron will summarize the major themes that emerge in the September essay. The lunches are also the informal start of our annual list of the Ten Surprises.

One out-of-consensus idea that I’ll propose this year is that U.S. growth and prices are not yet near their peak. Extreme volatility in macro and market data has begun to subside, with commodity prices coming down from heady levels and policy stimulus abating later this year, notwithstanding the likely passage of an infrastructure bill. These dynamics led some market watchers to pronounce the death of the reflation trade. Just look at the Treasury market, where the 10-year is about 40 basis points lower due to expectations of slower growth and lower long-term inflation.

But these days, I’m paying less attention to growth rates, which were always bound to slow from their breakneck pandemic speeds. In fact, I think the continuing correction in materials prices and easing of supply-chain constraints represent future tailwinds for economic growth because they will help resolve supply and demand mismatches. More important to watch are activity levels, which remain well-supported by healthy consumers, corporations, and state and local governments. I expect strong economic activity will drive the successful handoff of the recovery from policy to fundamentals, as I discussed in June.

How Much Is That Condo on the Corner?

One area facing data volatility and growth concerns is the U.S. housing market, where supply and demand have struggled to find equilibrium and prices have soared since summer 2020. Anecdotes abound of tight housing markets, featuring bidding wars and cash-only offers. In a dystopian turn that would’ve been unimaginable 18 months ago, some brokers are selecting buyers via Powerball-style drawings held over Zoom.1

Outsized demand, driven by three factors… First, COVID lockdowns fueled the continuation of migratory patterns to the U.S. South and West, where mid-sized cities and suburban communities offer more space at lower prices than denser urban areas. Second, government transfers and limited spending opportunities boosted cash savings; for some, this scenario finally made a down payment affordable. Third, mortgage rates remain at historic lows: the 30-year fixed rate is below 3% even as the economy grows and prices climb.2

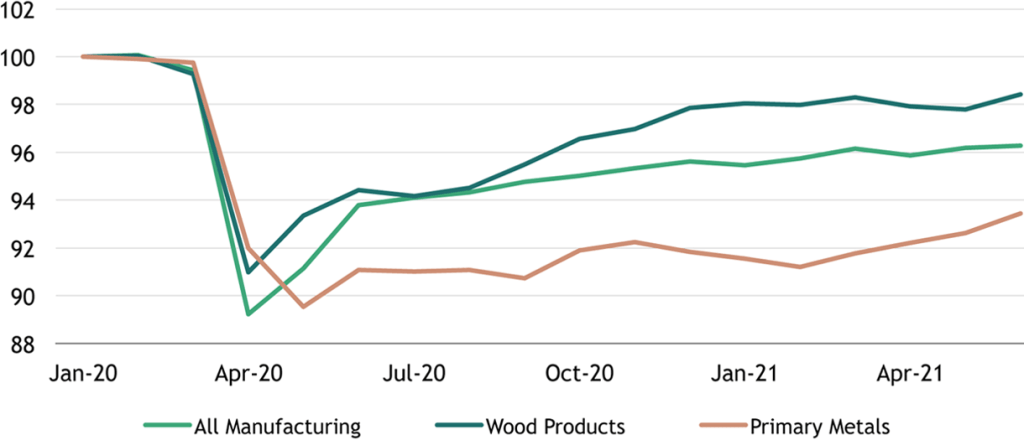

…presses up against limited supply Soaring commodity prices and limited labor supply mean construction costs more. Early in the global reopening, unloaded shipping containers sat on ships stuck at sea, waiting for berths at ports. Lumber prices surged as sawmills struggled to meet demand from construction companies and Americans’ home improvement projects. Also, U.S. manufacturing jobs struggled to rebound during the summer and fall of 2020, resulting in fewer workers available to churn out pine boards and nails (see Figure 1).

Figure 1: All Employees, Select Manufacturing Sectors

(indexed to 100 as of January 2020, seasonally adjusted)

Source: Blackstone Investment Strategy and U.S. Bureau of Labor Statistics, as of 6/30/2021.

Prices up, sentiment down The consequences of this supply and demand mismatch are visible in the housing market. The median price of a new single-family home increased on a year-over-year basis by 22% in April 2021 and another 20% in May, before moderating to 6% in June. Existing home prices were up a whopping 23.4% year-over-year in June and reached a record high of $363,300.3 Given this price pressure, the percentage of people who think conditions are good for buying a house are at their lowest level since 1982, when mortgage rates were above 14% and inflation was in double digits.4 In June, new and existing homes sales slowed, a downside surprise.

If it looks, swims, and quacks like a bubble… Also soaring are Google searches for phrases like “Are we in a housing bubble?” And it’s not just casual market watchers who are starting to worry. Boston Federal Reserve President Eric Rosengren expressed concern in June about house prices and the Fed’s continued pace of mortgage-backed security (MBS) purchases. He warned of “too much exuberance,” and he urged policymakers and investors to “pay close attention to what’s happening in the housing market.”5

Thematic Conviction in Housing Activity

Despite high prices and negative sentiment, I’m still positive on housing activity over the coming decade. This is not to say that house prices will continue to grow at the rapid rates seen since last summer. Rather, I think that fading pandemic constraints will help boost supply while household formation and demographic tailwinds encourage strong demand. I expect this equilibration to support continued growth in house building and buying at a healthier, more sustainable pace, with positive implications for real economic growth.

Housing supply will improve Importantly, I expect materials prices to normalize as supply chain constraints continue to alleviate over the next 1–2 years. The July 2021 lumber futures contract increased 373% from May 2020 to May 2021; since then, it’s down 59%.6 I think this is a combination of lower demand (eased restrictions in the U.S. mean fewer at-home carpentry projects) and higher supply (sawmills have had multiple months to begin to rebuild capacity). Global supply chains should also ease up as manufacturing production revives, more dock workers are hired, and shipping lanes resume their pre-pandemic flow.

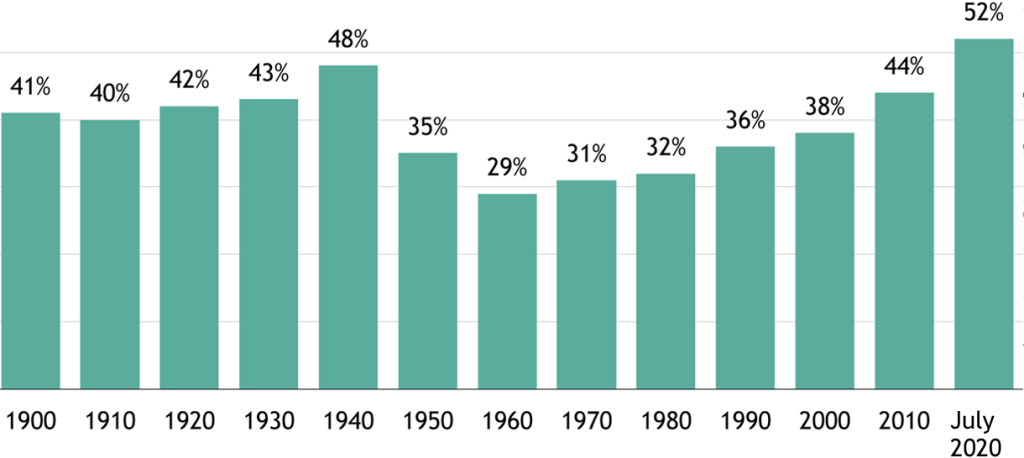

The millennials are coming! On the demand side, a secular trend to watch is the behavior of young adults, who disproportionately moved home to live with their parents during COVID. In 2020, the percentage of young adults living at home was the highest in the history of this metric (see Figure 2). I expect this pattern to reverse as the U.S. exits the pandemic and millennials age. Almost 5 million millennials will turn 30 each year from 2021 through 2024 and enter prime home-buying age.7 But they won’t be able to move into houses vacated by their elders: Baby Boomers have held the largest and most stable share of real estate wealth of any American generation for the past 20 years.8 That suggests that more houses will have to be built for younger Americans to have a shot at their own homestead.

Figure 2: U.S. Young Adults Living with a Parent

(share of total population aged 18-29)

Source: Blackstone Investment Strategy and Pew Research Center. Represents young adults residing with at least one parent in the household. 1900-1990 shares based on household population as measured in the decennial census. Observations for 2000 and 2010 represent the aggregation of annual averages from the Current Population Survey. Observation for July 2020 is from the 2020 Current Population Survey monthly files (IPUMS).

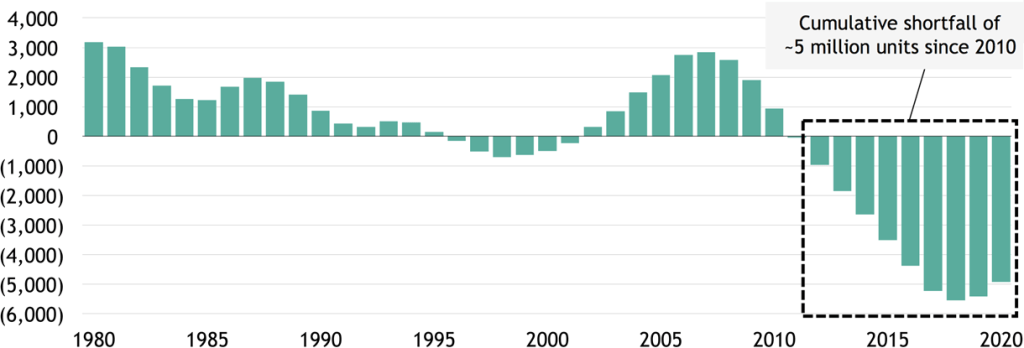

Such housing demand will help to reverse another multi-year trend. After the bubble and bust that preceded the Global Financial Crisis, U.S. housing entered a period of chronic underbuilding. A recent report estimates that the housing “underbuilding gap” is between 5.5 million and 6.8 million units since 2001 (see Figure 3).9

Figure 3: Surplus (Shortfall) of New Home Completions, Relative to Historical Average

(thousands of units, rolling 10-year sum)

Source: Blackstone Investment Strategy, U.S. Census Bureau, and U.S. Department of Urban Housing and Development, as of 5/31/2021. “New Home Completions” is the number of total new privately owned housing units completed in each calendar year, calculated as the average of monthly units completed at a seasonally adjusted annual rate. The “Historical Average” is the average of annual housing completions from 1968 to 2020.

This gap has contributed to steadily declining inventories of houses for sale, which hit rock-bottom at the end of 2020. There has also been secular under-building of new multifamily apartment buildings. By my team’s calculation, there has been a cumulative shortfall of around 1.1 million multifamily housing units since 2010, compared to the historical average.10 Housing construction tends to move in sinusoidal patterns, and I think the last decade’s undershoot, combined with new demand coming from younger generations, signals the beginning of a new building cycle.

Mortgage rates in a post-taper world Byron and I expect interest rates to structurally increase during the recovery. In our view, the current distortion in Treasury markets from the Fed’s quantitative easing will be resolved when tapering begins in early 2022. The tapering will drain excess demand from fixed income markets, and yields will back up. And when that happens, mortgage rates are likely to climb from their current nadir. However, they have plenty of room to rise relative to historical levels.

Also, it’s important to remember that most people have two housing choices: they can buy or rent. The U.S. housing shortfall will take years to reverse, especially given that new residential construction takes longer today than it once did. The average amount of time required to receive authorization for and complete construction on a single-family home rose to a combined 7.8 months in 2020, one of the highest levels on record and the highest since 2010.11 Given these constraints, many would-be buyers will opt to rent, especially in areas experiencing secular demographic tailwinds with massive demand and supply that has yet to ramp up. Such areas include the “Smile States” in the South and Southwest, which generally have lower density and lower cost of living than their coastal counterparts. As a likely sign of things to come, a pandemic recovery for rent prices is underway, which should be a source of “sticky” inflation over the coming cycle.

An Investor’s Guide to a Sustainable Housing Cycle

As housing activity strengthens, multiplier effects will roll through the U.S. economy. And I would encourage investors to consider whether their portfolios are positioned to benefit from them.

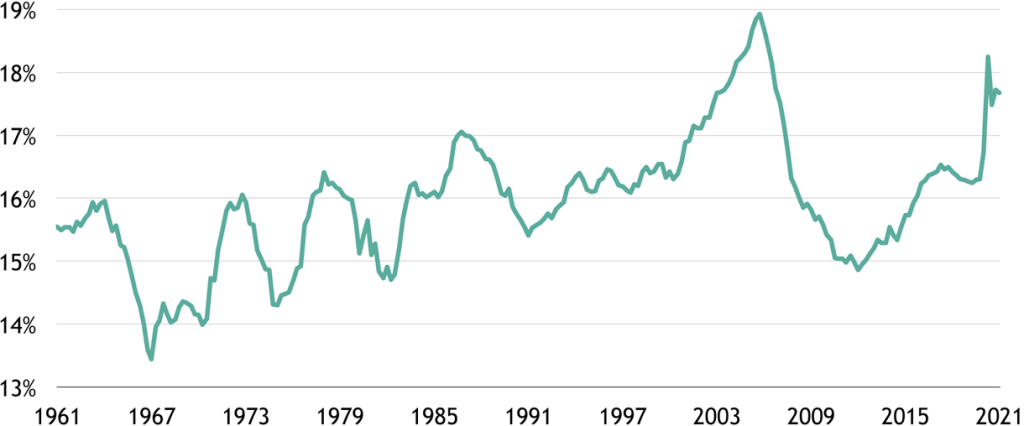

IKEA: for the home too, not just meatballs The housing market pulls two main levers of expenditure. The first is spending on construction, remodeling, and brokers’ fees, which we call residential fixed investment. The second is spending on rents, utilities, and homeowner-imputed rent and utility payments. Joint spending in these two areas as a share of U.S. GDP soared to almost 19% during the housing bubble of the early 2000s, plunged during the financial crisis and, as of 1Q21, climbed back up to 17.7% (see Figure 4). I think that healthy household balance sheets, boosted by a level of fiscal stimulus that the U.S. hasn’t seen since World War II, will help this spending set a new high in the coming cycle.

Figure 4: Spending on U.S. Housing

(percentage of GDP, seasonally adjusted)

Source: Blackstone Investment Strategy and U.S. Bureau of Economic Analysis, as of 3/31/2021. Represents combined spending on private residential fixed investment and on housing and utilities (as a component of Personal Consumption Expenditures) as a share of nominal U.S. GDP.

Real estate activity has large positive knock-on effects that ripple through the economy. One estimate shows that for every $1 million in output from the real estate and rental leasing sector, 22.6 jobs are created, over 90% of which are indirect—the highest employment multiplier of any sector.12 Poised to benefit from continued strength in housing are the manufacturing and construction companies that will be enlisted to build new houses. And with every new house comes a flood of discretionary spending: Americans spent $112 billion on furnishings and durable household equipment in 1Q21, which works out to $800 for each of the 140 million houses in the U.S.

Insights from our portfolio My team and I often work with Blackstone’s acquisition teams to help them think through sectors with broad exposure to macro trends. And two of the firm’s recently announced acquisitions reflect my view that the dual secular trends of homebuilding and homebuying are likely to continue. In February, the firm announced that private equity funds managed by Blackstone agreed to acquire Interior Logic Group Holdings, a data-driven provider of interior design, supply chain, and installation management solutions to some of the country’s largest single-family home builders. And in June, a real estate vehicle managed by Blackstone announced plans to acquire Home Partners of America (HPA), which owns more than 17,000 houses across the United States. Many people may want to live in a single-family home but may not yet be ready to purchase their own house. These individuals can work with a realtor to select a property, which HPA will then purchase and rent back to them. Most importantly, the tenants have the right to buy the property from HPA in the future.

My team and I also benefit from the firm’s asset management teams’ on-the-ground insights into pockets of strong performance. Currently, one such pocket is suburban markets. Tailwinds including lower prices, greater space, and cheaper taxes have produced migratory patterns to the South and West that pre-date (but were accelerated by) the pandemic. And it’s not just sales markets—rental markets are thriving, too. As high-income earners have migrated to the suburbs, they’ve found roomier homes that cost them a smaller share of their income, even in expanding neighborhoods. In fact, our internal data show that national rent-to-income ratios have fallen slightly over the last 18 months for new residents across the Blackstone real estate portfolio.13

Another strong trend as the pandemic eases is re-urbanization, especially in “gateway” cities like Seattle and Denver. The pandemic severely affected housing and rental markets in these areas as people left cities en masse. Some pundits even opined that the U.S. city was dead, as businesses, cultural institutions, and public transit turned off their lights. However, following a strong national vaccine uptake and lifted lockdowns, demand is recovering even in the densest markets. In New York City, there were more new rental leases signed this June than in any previous month since at least 2008.14 Looking at Blackstone Real Estate’s holdings, lease applications for a segment of our portfolio in New York City were up 115% in July 2021, compared to the same period in 2019.15

Just as Blackstone’s investments are premised on strong housing activity, aided by important demographic developments, investors should consider looking for ways to similarly expose their own portfolios to rising rents, house building, and demand for property ownership by young Americans. Because house price growth doesn’t have to maintain its rapid pace for housing markets to remain healthy.

With data and analysis by Taylor Becker.

- New York Times, as of 5/29/2021.

- Freddie Mac, as of 7/8/2021.

- U.S. Census Bureau, as of 6/30/2021 (new homes); National Association of Realtors, as of 6/30/2021 (existing homes).

- University of Michigan Consumer Survey, as of 6/30/2021. Represents the share of respondents answering “good” in response to the question, “Generally speaking, do you think now is a good time or bad time to buy a house?”

- Financial Times, as of 6/28/2021.

- Chicago Mercantile Exchange, as of 7/14/2021. Represents the price of the July 2021 random length lumber futures contract.

- Forbes, as of 2/17/2021.

- Federal Reserve Board of Governors, as of 6/21/2021.

- National Association of Realtors, as of 6/16/2021.

- Source: Blackstone Investment Strategy, U.S. Census Bureau, and U.S. Department of Urban Housing and Development, as of 12/31/20. “Multifamily” represents total units less single-family units. The “historical average” is the average of annual housing completions from 1968 to 2020. “Cumulative shortfall” represents the difference between annual multifamily housing completions and the historical average, summed over the ten-year period from 2010-2020.

- Census Bureau, as of 12/31/2020.

- Economic Policy Institute, as of 1/23/2019. Indirect jobs include “supplier jobs” (materials and capital services supplier jobs) and “induced jobs” (jobs supported by respending of income from direct jobs and supplier jobs, as well as public sector jobs supported by tax revenue).

- Blackstone and LivCor Proprietary Data, as of 6/25/2021.

- Douglas Elliman, as of 6/30/2021.

- Blackstone Proprietary Data, as of 7/28/21.

The views expressed in this commentary are the personal views of Joe Zidle and do not necessarily reflect the views of The Blackstone Group Inc. (together with its affiliates, “Blackstone”). The views expressed reflect the current views of Joe Zidle as of the date hereof, and neither Joe Zidle nor Blackstone undertake any responsibility to advise you of any changes in the views expressed herein.

Blackstone and others associated with it may have positions in and effect transactions in securities of companies mentioned or indirectly referenced in this commentary and may also perform or seek to perform services for those companies. Blackstone and others associated with it may also offer strategies to third parties for compensation within those asset classes mentioned or described in this commentary. Investment concepts mentioned in this commentary may be unsuitable for investors depending on their specific investment objectives and financial position.

Tax considerations, margin requirements, commissions and other transaction costs may significantly affect the economic consequences of any transaction concepts referenced in this commentary and should be reviewed carefully with one’s investment and tax advisors. All information in this commentary is believed to be reliable as of the date on which this commentary was issued, and has been obtained from public sources believed to be reliable. No representation or warranty, either express or implied, is provided in relation to the accuracy or completeness of the information contained herein.

This commentary does not constitute an offer to sell any securities or the solicitation of an offer to purchase any securities. This commentary discusses broad market, industry or sector trends, or other general economic, market or political conditions and has not been provided in a fiduciary capacity under ERISA and should not be construed as research, investment advice, or any investment recommendation. Past performance is not necessarily indicative of future performance.

Blackstone Proprietary Data. Certain information and data provided herein is based on Blackstone proprietary knowledge and data. Portfolio companies may provide proprietary market data to Blackstone, including about local market supply and demand conditions, current market rents and operating expenses, capital expenditures, and valuations for multiple assets. Such proprietary market data is used by Blackstone to evaluate market trends as well as to underwrite potential and existing investments. While Blackstone currently believes that such information is reliable for purposes used herein, it is subject to change, and reflects Blackstone’s opinion as to whether the amount, nature and quality of the data is sufficient for the applicable conclusion, and no representations are made as to the accuracy or completeness thereof.

Trends. There can be no assurances that any of the trends described herein will continue or will not reverse. Past events and trends do not imply, predict or guarantee, and are not necessarily indicative of, future events or results.