Joe Zidle: A Real-World Investment in the Age of AI

Bubble speculation is something of a sport in Wall Street circles. After all, to be first in identifying any form of excess can be wildly profitable. Being the next Jeremy Grantham, often acknowledged for predicting the 1999 tech bubble, or Michael Burry, he of the housing bubble prophecy in 2007 that earned him recognition in books and film, has significant appeal. But their accurate predictions are clear exceptions in bubble speculation history. So, when I see more and more reports questioning whether there’s a generative AI bubble, I view them with a skeptical eye.

When analyzing a sector for potential excess in the market, we have to look at its foundation, deeper than recent performance and hype. AI’s foundation is data and the infrastructure required to use it, which is one reason that leads me to believe that this isn’t a bubble. It’s a developing long-term growth opportunity across a potentially transformative technology value chain.

It’s early days of AI’s growth story At Blackstone, we recently assembled a network of chief technology officers to discuss, among other topics, AI’s impact and its potential. A common observation from these CTOs is that many companies are in the research phase with AI and have yet to fully exploit its capabilities for productivity. I believe these discussions leave little doubt that generative AI will bring about monumental transformations, but it will do so in ways that we cannot yet fully understand.

Yes, AI-related stocks have surged significantly this year. But as Deutsche Bank Research Strategist Jim Reid humorously noted in his “Flippant Friday” post, if this were the trajectory of AI stocks with only 50% public awareness, where will these stocks land when the entire population becomes aware of AI?

Where we are currently is the beginning of businesses and the wider economy integrating AI. With as many, if not more, questions than answers currently, what we can do is look to identify the dynamics that figure to be integral to AI’s implementation and growth trajectory.

More data means more storage needed In some respects, generative AI reminds me of the earliest days of e-commerce growth. It was clear that Amazon would fundamentally disrupt the retail industry, and that sent investors hunting for the infrastructure that would enable its success. Not so obvious initially was that warehouses would be integral to Amazon’s rise. To fulfill its promise, Amazon needed last-mile distribution, which required a massive amount of warehouse capacity near population centers. Urban in-fill warehouses were transformed.

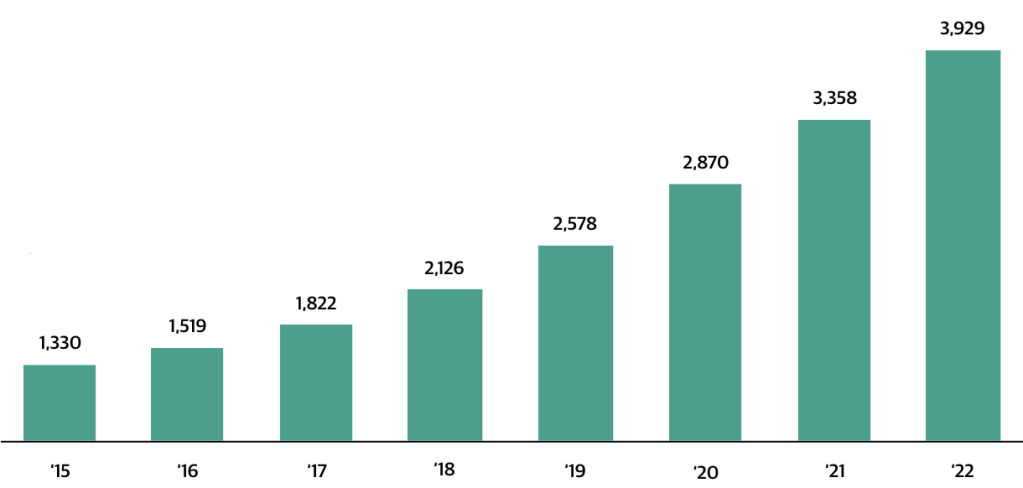

Today, we can look at AI and data centers the same way. Generative AI models rely on robust data processing capabilities and extensive storage capacities, which should drive demand for physical data centers that can handle the intensive computational requirements of generative AI applications. Also, data centers enable distributed training and inference, efficiently coordinating operations across multiple machines or multiple other data centers. The demand for data centers has increased dramatically in recent years with storage and computing requirements shifting to the cloud. According to CBRE estimates shown in Figure 1, data center inventory has nearly tripled since 2015.1

Figure 1: Data Center Primary Market Total Inventory (MW)

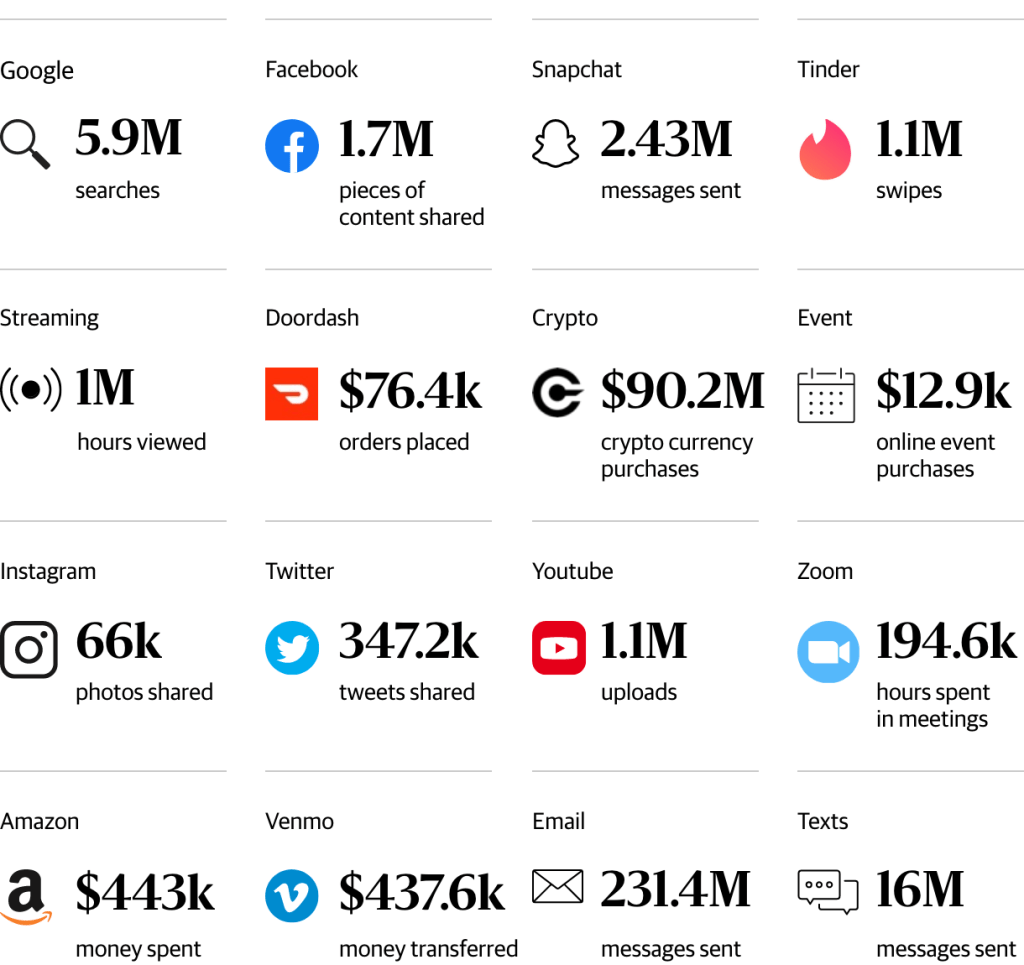

This data center growth really should come as no surprise considering the sheer mass of data that the world now produces each day. Figure 2 shows some mind-blowing examples, like that more than 230 million emails and 16 million texts are sent every minute of every day. Each minute also yields 5.9 million Google searches, 1.7 million pieces of content shared on Facebook, and 347,000 Tweets shared on Twitter.

Figure 2: Amount of Data Generated Each Minute of the Day

Opportunities in generative AI’s physical presence Now add AI to the mix. It’s natural to think of AI as an esoteric, abstract concept; a form of software that lives in the ether. In reality, real world data centers anchor AI, just as they do data storage and cloud-based applications that run on physical servers. The physical needs of AI will diverge in certain ways from existing applications and could lead to the development of data centers tailored for the new technology. Meta, for example, recently shared details on its own plans to redesign data centers projects to support its AI development.

Data demand multiplier The same impetus drives the many competing forces racing to develop both narrow and broad generative AI models. All of them heavily rely on substantial computational power, robust data processing capabilities, and extensive storage capacities. All of them are expected to drive increasing demand for data centers that are foundational to handling those intensive requirements to power generative AI applications. Moreover, data centers enable distributed training and inference, efficiently coordinating operations across multiple machines or data centers.

We may not fully understand the costs and benefits of generative AI, but I believe that it is here to stay and that it will bring a surge of investment into the field. While the tech companies battle over the development potential and applications, from my perspective, data centers seem well-positioned to thrive in the present and future of an AI-driven world.

With data and analysis by Taylor Becker.

The views expressed in this commentary are the personal views of Joe Zidle and Taylor Becker and do not necessarily reflect the views of Blackstone Inc. (together with its affiliates, “Blackstone”). The views expressed reflect the current views of Joe Zidle and Taylor Becker as of the date hereof, and neither Joe Zidle, Taylor Becker, or Blackstone undertake any responsibility to advise you of any changes in the views expressed herein.

Blackstone and others associated with it may have positions in and effect transactions in securities of companies mentioned or indirectly referenced in this commentary and may also perform or seek to perform services for those companies. Blackstone and others associated with it may also offer strategies to third parties for compensation within those asset classes mentioned or described in this commentary. Investment concepts mentioned in this commentary may be unsuitable for investors depending on their specific investment objectives and financial position.

Tax considerations, margin requirements, commissions and other transaction costs may significantly affect the economic consequences of any transaction concepts referenced in this commentary and should be reviewed carefully with one’s investment and tax advisors. All information in this commentary is believed to be reliable as of the date on which this commentary was issued, and has been obtained from public sources believed to be reliable. No representation or warranty, either express or implied, is provided in relation to the accuracy or completeness of the information contained herein.

This commentary does not constitute an offer to sell any securities or the solicitation of an offer to purchase any securities. This commentary discusses broad market, industry or sector trends, or other general economic, market or political conditions and has not been provided in a fiduciary capacity under ERISA and should not be construed as research, investment advice, or any investment recommendation. Past performance is not necessarily indicative of future performance.

For more information about how Blackstone collects, uses, stores and processes your personal information, please see our Privacy Policy here: www.blackstone.com/privacy. You have the right to object to receiving direct marketing from Blackstone at any time. Please click the link above to unsubscribe from this mailing list.