Joe Zidle: Unintended Consequences of a Dovish Shift

Markets rallied significantly over the past week on the US election outcome and remarkable vaccine progress. The vaccine news gives great cause for hope that we may finally be entering a period that feels more familiar than this turbulent year we’ve all endured. But the timeline for approval and distribution is not knowable at this time, so it is especially important that policymakers strike the right balance between fiscal and monetary policy in order to support this fragile economic recovery. Fiscal policy that is not adequately supportive could cause the Fed to turn even more dovish.

Scaled-back fiscal goals The unrealized Blue Wave was expected to deliver massive fiscal stimulus in 2021. Some analysts estimated that the increased government spending would lift US GDP growth by 1.3% to 1.5% next year.1 But any further fiscal support is almost certain to be scaled back in a split-government scenario. As a result, monetary policy will have to step up.

Spending, not lending The Fed is likely to remain highly accommodative, but access to capital isn’t the problem. Through August, US companies issued $1.9 trillion in debt and another $310 billion in equity.2 In just 8 months this year, debt and equity issuance have already broken the full-year records set in 2017 and 2000, respectively.1 Insufficient credit isn’t the issue; it’s demand. Zero rates can’t replicate demand in economies with aging populations and weak investment. Europe and Japan have demonstrated that.

Two Critical Unintended Consequences

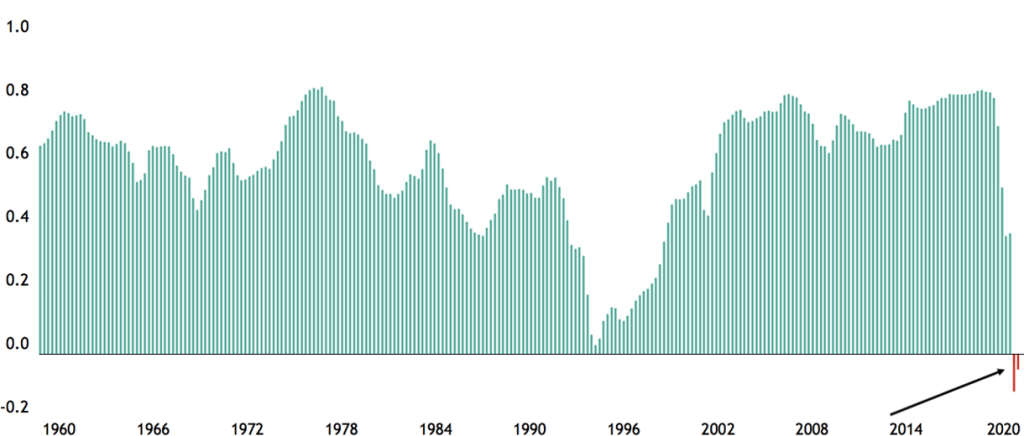

The Disconnected Bull Market Low rates and quantitative easing (QE) didn’t produce much in the way of demand growth or investment in the last economic cycle. From 2010–2019, US real GDP growth averaged just 2.3%, relative to the trailing 50-year average of 3.5%. Inflation also undershot consistently. But where liquidity failed in lifting the real economy, it succeeded in reflating financial assets. That’s why markets have become disconnected from the economy, arguably for the first time in modern history (see Figure 1). The liquidity that facilitated these conditions shows no sign of receding.

Figure 1: 10-Year Correlation between S&P 500 and US GDP

Source: Cornerstone Macro, as of 9/30/20. Represents rolling 10-year correlation between quarterly year-over-year change in S&P 500 total return index and quarterly year-over-year change in US real GDP, two quarter lead.

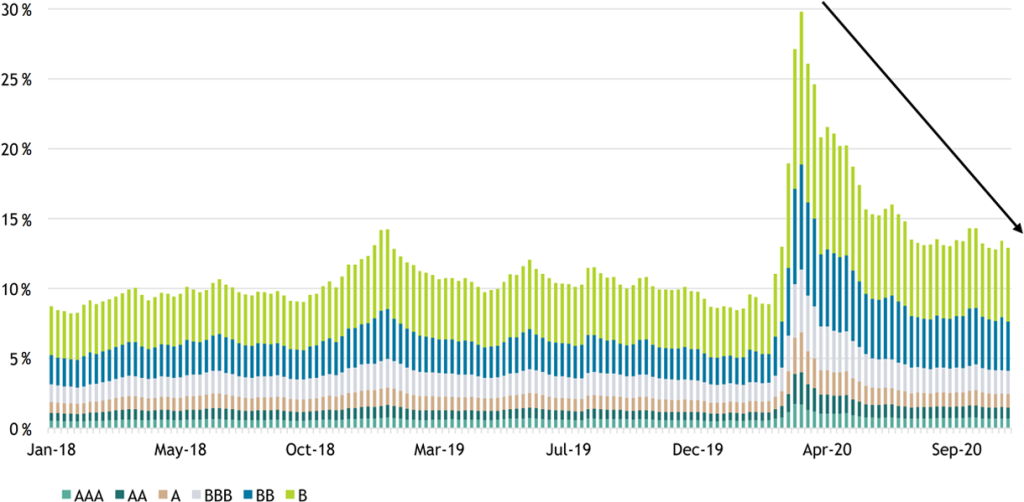

Creating a Scarcity of Yield As the Fed relies on zero rates and QE, the yields of many fixed income products will continue to fall, in my view. And investors will continue to get increasingly less yield for the same levels of risk. In public markets, spreads have nearly tightened back to pre-COVID levels (see Figure 2). Last Monday, coupons on high yield bonds were just 18 basis points away from the record low reached in 2014.3 This, despite record high corporate debt levels, weaker earnings and a record number of non-earning companies. These trends are unlikely to reverse soon. Fed Chair Powell says that monetary policy risk is “asymmetric”—doing too little is more dangerous to the economy than overdoing it.4

Figure 2: Corporate Bond Index Spread Pickup by Rating Tier

Source: ICE BofA Indices, as of 11/6/20. ICE BofA indices track the performance of US dollar denominated investment grade and high-yield corporate debt publicly issued in the US domestic market. Spread data represents the option-adjusted spread, which are the calculated spreads between a computed OAS index of all bonds in a given rating category and a spot Treasury curve. An OAS index is constructed using each constituent bond’s OAS, weighted by market capitalization.

Evolving Asset Allocation In this environment, the traditional 60/40 portfolio will come under further pressure. I highlighted the role of private real estate, private credit and alternatives in portfolios, and the attractive yields relative to public fixed income. My preferred private real estate sectors include industrial, self-storage and life sciences, which have had stable cap rates this year while the 10-year Treasury yield halved.5 In private credit markets, sectors with secular tailwinds such as tech, software and logistics are particularly attractive relative to capital-intensive cyclical businesses.

Investors must consider the unintended consequences of the Fed’s role in reflating the economy. For the challenging environment ahead, I believe thematic and high-conviction investing are poised to shine.

With data and analysis by Taylor Becker.

1. Goldman Sachs and BX calculations, as of 9/21/20

2. Refinitiv and Financial Times, as of 9/2/20. https://www.ft.com/content/a59c2a9d-5e0b-4cbc-b69e-a138de76a776

3. Bloomberg, as of 11/9/20.

4. Federal Reserve, as of 10/6/20: https://www.federalreserve.gov/newsevents/speech/powell20201006a.htm

5. Greenstreet, BX calculations. As of 10/1/20.

The views expressed in this commentary are the personal views of Joe Zidle and do not necessarily reflect the views of The Blackstone Group Inc. (together with its affiliates, “Blackstone”). The views expressed reflect the current views of Joe Zidle as of the date hereof, and none of Joe Zidle nor Blackstone undertake any responsibility to advise you of any changes in the views expressed herein.

Blackstone and others associated with it may have positions in and effect transactions in securities of companies mentioned or indirectly referenced in this commentary and may also perform or seek to perform services for those companies. Blackstone and others associated with it may also offer strategies to third parties for compensation within those asset classes mentioned or described in this commentary. Investment concepts mentioned in this commentary may be unsuitable for investors depending on their specific investment objectives and financial position.

Tax considerations, margin requirements, commissions and other transaction costs may significantly affect the economic consequences of any transaction concepts referenced in this commentary and should be reviewed carefully with one’s investment and tax advisors. All information in this commentary is believed to be reliable as of the date on which this commentary was issued, and has been obtained from public sources believed to be reliable. No representation or warranty, either express or implied, is provided in relation to the accuracy or completeness of the information contained herein. This commentary does not constitute an offer to sell any securities or the solicitation of an offer to purchase any securities. This commentary discusses broad market, industry or sector trends, or other general economic, market or political conditions and has not been provided in a fiduciary capacity under ERISA and should not be construed as research, investment advice, or any investment recommendation. Past performance is not necessarily indicative of future performance.