Joe Zidle: Waiting on a Fed Pivot Can Lead to Missed Opportunities

In a world of moderating inflation and slowing economic growth, I understand why it may be tempting for investors to assume that the Federal Reserve (Fed) will pivot quickly and ease its monetary policy. However, I believe that it is essential to resist this temptation, as the facts on the ground don’t suggest a Fed shift is imminent. Investors would be better served focusing on strategic positioning for an extended period of higher rates.

Labor market pushes back against Fed pivot case Inflation has undoubtedly peaked. Shelter was the primary contributor on the way up and is soon to drive further disinflation. Market data for rents and home prices had suggested a turnaround in shelter prices was coming soon, and the latest data for March finally showed the first slowdown in the Consumer Price Index (CPI) for shelter since it started accelerating.

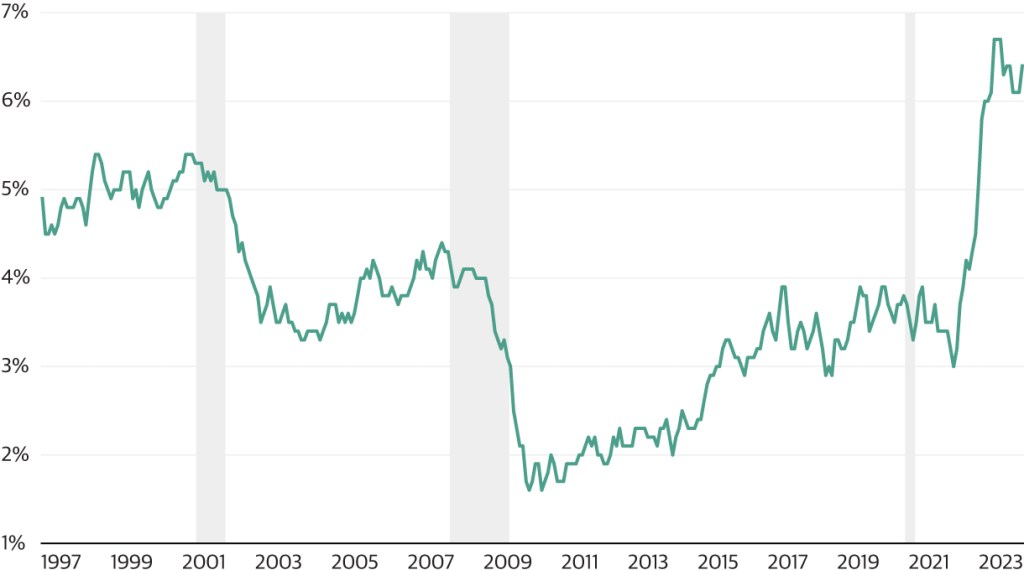

To be sure, we are nearing the end of the Fed’s hiking cycle. But disinflation alone is not enough to cause a swift pivot in policy, which is why it’s important to highlight the ongoing strengths in the labor market that may frustrate interest rate doves. Notably, wage growth has not eased to levels that are consistent with the Fed’s inflation targets. Initial jobless claims data are beginning to rise substantially after touching some of the lowest levels since the late 1960s; however, wage pressure remains acute. The chart below highlights the Atlanta Fed’s wage growth tracker which focuses on wage growth for individuals over time, reflecting the median percent change in the hourly wages of individuals observed 12 months apart, and controls for issues like mix-shift in a way that measures like Average Hourly Earnings cannot.

Figure 1: Atlanta Fed’s Wage Growth Tracker

(3-month moving average, hourly data)

Source: Federal Reserve Bank of Atlanta and Bloomberg, as of 3/31/2023.

Attempting to pinpoint the exact moment of the Fed’s pivot is, as John Maynard Keynes once quipped, like trying to predict when “the ocean is flat again” after a storm has passed. But we can still try and ascertain what might need to happen for the Fed to start to reverse course. An almost sure-fire catalyst would be a significant and rapid reversal of extremely tight labor markets.

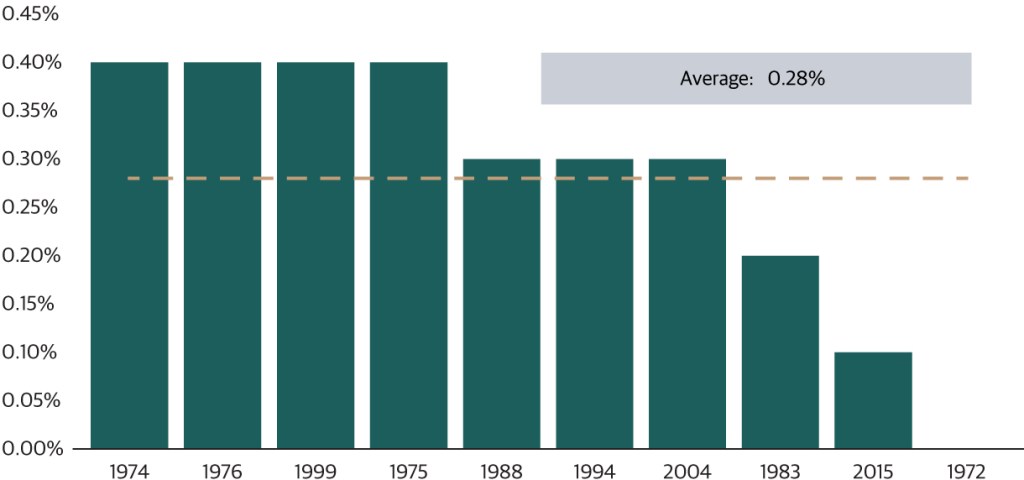

When looking at prior Fed cycles, the amount of time between the last hike and the first cut is variable, but unemployment is a critical determinant. Historically, when the unemployment rate has risen by an average of 28bps from the cycle low, the Fed begins to cut rates. This time, though, joblessness is troughing at an ultra-low level. As such, the Fed may tolerate a greater increase in unemployment this time around.

Figure 2: US Unemployment Rate

(change from cycle low to first Fed rate cut)

Source: Blackstone Investment Strategy Calculations, Federal Reserve, US Bureau of Labor Statistics and Bloomberg, as of 3/31/2023. Data reflects the change in US unemployment rate from its respective trough in each hiking cycle to the first Fed rate cut. Fed hiking cycle dates are based on the first Fed rate hike to the last rate hike and are defined as follows: March 1972 – August 1973; March 1974 – May 1974; June 1975 – May 1976; December 1976 – October 1979; March 1983 – August 1984; March 1988 – May 1989; February 1994 – February 1995; June 1999 – May 2000; June 2004 – June 2006 and December 2015 – December 2018. The trough in the unemployment rate took place on the following dates: August 1973, May 1974, May 1976, May 1979, June 1984, March 1989, March 1995, April 2000, May 2007, and June 2019. The first Fed rate cuts following each respective hiking cycle took place on the following dates: September 1973, July 1974, July 1976, December 1979, October 1984, June 1989, July 1995, January 2001, September 2007, and July 2019.

Higher for longer rates call for strategic positioning As allocators and investors, our goal is not to predict the Fed’s next move, but rather to focus on what we do know and adapt our investment strategy accordingly. So instead of waiting on the Fed, which continues to see persistent labor market strength and uncertain disinflation, we believe positioning portfolios to weather higher rates for longer than the consensus or market pricing would suggest remains important.

At the same time, and even as top-line growth has held up relatively well, margin pressures are leading to slower profits growth in the overall economy. Compare this to the results from Blackstone’s 1Q CEO Survey, in which respondents were generally more upbeat. In this quarter’s survey, respondents expressed relative optimism about profit and revenue growth, and expectations of continued easing in inflationary pressures and relatively stable profit margins. To some extent, this reflects the importance of smart selection and active management in periods of dislocation and volatility.

In this environment, we prioritize higher quality and growing cash flow in preparation for a changing and uncertain landscape. While a 5% return in cash markets is appealing, we believe providing capital where it is scarce can yield some of the strongest long-term performance.

With data and analysis by Taylor Becker.

The views expressed in this commentary are the personal views of Joe Zidle and Taylor Becker and do not necessarily reflect the views of Blackstone Inc. (together with its affiliates, “Blackstone”). The views expressed reflect the current views of Joe Zidle and Taylor Becker as of the date hereof, and neither Joe Zidle, Taylor Becker, or Blackstone undertake any responsibility to advise you of any changes in the views expressed herein.

The Blackstone survey of a subset of portfolio company CEOs referred to herein reflects input from 76 Blackstone portfolio companies (52 U.S. CEOs), largely within Blackstone’s Private Equity and Real Estate businesses (the “CEO Survey”). The CEO Survey was initiated on March 6, 2023 and closed March 20, 2023. The responding portfolio companies are not necessarily a representative sample of companies across Blackstone’s portfolio. The views expressed by responding portfolio companies in the CEO Survey do not necessarily reflect the views of Blackstone.

Blackstone and others associated with it may have positions in and effect transactions in securities of companies mentioned or indirectly referenced in this commentary and may also perform or seek to perform services for those companies. Blackstone and others associated with it may also offer strategies to third parties for compensation within those asset classes mentioned or described in this commentary. Investment concepts mentioned in this commentary may be unsuitable for investors depending on their specific investment objectives and financial position.

Tax considerations, margin requirements, commissions and other transaction costs may significantly affect the economic consequences of any transaction concepts referenced in this commentary and should be reviewed carefully with one’s investment and tax advisors. All information in this commentary is believed to be reliable as of the date on which this commentary was issued, and has been obtained from public sources believed to be reliable. No representation or warranty, either express or implied, is provided in relation to the accuracy or completeness of the information contained herein.

This commentary does not constitute an offer to sell any securities or the solicitation of an offer to purchase any securities. This commentary discusses broad market, industry or sector trends, or other general economic, market or political conditions and has not been provided in a fiduciary capacity under ERISA and should not be construed as research, investment advice, or any investment recommendation. Past performance is not necessarily indicative of future performance.

For more information about how Blackstone collects, uses, stores and processes your personal information, please see our Privacy Policy here: www.blackstone.com/privacy. You have the right to object to receiving direct marketing from Blackstone at any time. Please click the link above to unsubscribe from this mailing list.